Debt By Default: Debt Collection Practices in Washington 2012–2016, A CRL Report Designed by Archetype

Archetype has helped create dozens of reports for the Center for Responsible Lending, since 2001. In March of 2019, we provided editing and graphic design for this 19-page report authored by CRL staff members Tom Feltner, Julia Barnard, and Lisa Stifler.

The report outlines how increases in consumer debt in recent decades have led to significant growth in the collection industry, of which debt buying is a subset. Debt buyers purchase debts from lenders and other creditors at a steep discount. They then attempt to collect the debt themselves, often using litigation. Previous research has established that debt buyers often abuse legal channels and that consumers are denied the opportunity to defend themselves.

The key findings of the report are as follows:

• Consumers and servicemembers in Washington have raised significant concerns about improper debt collection practices. An analysis of complaints to the CFPB shows that debt collection complaints are the second most common type made by Washingtonians, and the most common type filed by Washington’s servicemembers.

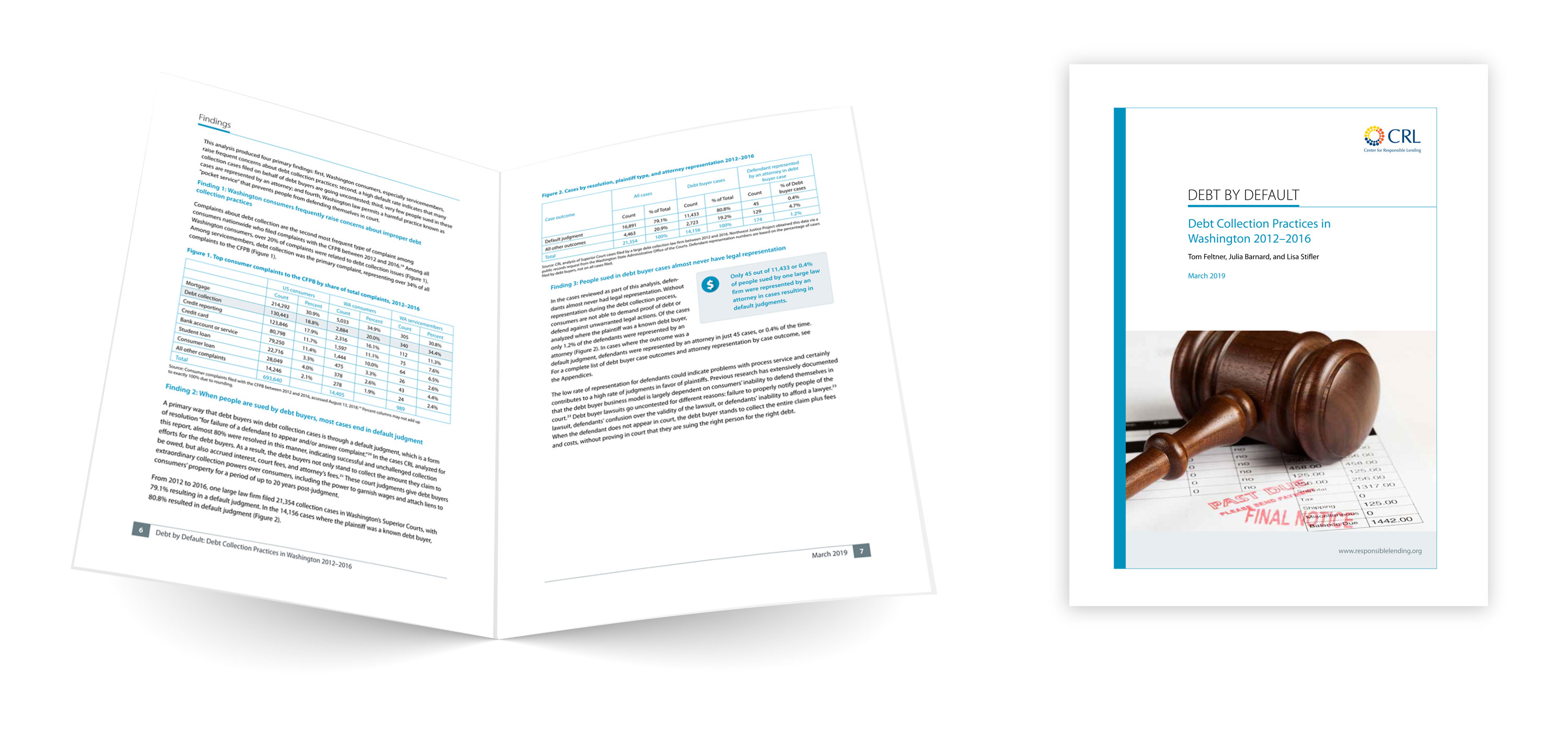

• Most debt buyer cases result in default judgments. Over 80% of all debt buyer cases reviewed resulted in default judgments in favor of the plaintiff. The prevalence of default judgments indicates successful and unchallenged collection efforts for the debt buyers reviewed in this study. For people sued by debt buyers, this means they are subject to a judgment or garnishment order without the debt buyer ever proving their case or the validity of the debt.

• Consumers almost never have representation. From 2012–2016, one large law firm frequently representing debt buyers filed 21,354 collection cases in Washington’s Superior Courts. Only 1.2% of defendants were represented by an attorney, and in cases where the outcome was a default judgment, defendants were represented in just 45 cases (0.4% of the time). Without being present or represented in court, consumers are not able to demand proof of debt or defend against unwarranted legal actions.

• “Pocket service” may be occurring in almost 70% of the cases reviewed. In Washington, a summons can be delivered prior to the case actually being filed in a practice called “pocket service.” Individuals served must respond within 20 days or they are in default—a time frame that applies even if no court case actually exists. Of the cases reviewed, nearly 70% were both filed and resolved with a default judgment within 20 days, indicating that many of these cases were likely subject to pocket service.

This report concludes with recommendations to address these practices that put consumers at a disadvantage:

• Ensure debt buyers prove that the debt is owed in court. Debt buyers should not be permitted to bring lawsuits against consumers unless they first meet a “proof of debt” standard. “Proof of debt” must be established through detailed information and original account-level documentation about the consumer and the debt. Examples include: full name, account numbers, original creditor’s name, itemization of the amount owed, the contract or account document indicating the consumer legitimately incurred the debt, and documentation establishing the debt buyer’s ownership of the debt (e.g., purchase and sale agreement).

• End the practice of “pocket service,” or serving individuals with debt collection lawsuits without actually filing the case in court. People facing debt collection lawsuits should be able to verify that the purported case summons they receive is not a sham. Debt collectors should not be able to proceed to judgment on any complaint that did not, at the time of service, bear a court-assigned case number.

• Discourage debt buyers from acting as “lawsuit factories” by holding them accountable for initiating unwarranted legal actions. Debt buyers should not be able to obtain judgments in cases where they bring unsubstantiated legal actions. Moreover, because of the harms these lawsuit mills inflict on people subject to collection actions, debt buyers should face monetary penalties if they pursue collection actions, including court cases against consumers, without first meeting the “proof of debt” standard.

• Require that debt buyers substantiate their claims made during collection attempts even before they sue. Debt buyers should be prohibited from attempting to collect a debt without having detailed information about the consumer and the debt, as well as original account-level documentation establishing the “proof of debt.” Debt buyers should be required to cease collection attempts if they cannot provide consumers with documents supporting the claimed debt upon request.

• Prohibit the collection of time-barred debts and other “zombie” debts. Washington law prohibits debt collectors from filing lawsuits on time-barred debt. Current law, however, allows collectors to attempt to collect these debts and to revive the stale debt by persuading the debtor to make a partial payment or otherwise affirm that the debt is owed. Debt buyers should be prohibited from restarting the clock on this type of debt by extracting payments or other affirmations from the consumer. Nor should they be allowed to collect on debts that are past the statute of limitations. Similarly, debt buyers should be banned from filing lawsuits or otherwise collecting on “zombie” debts—debts that have already been paid, settled in full, or discharged in bankruptcy.